Five years of HMRC customer redress data paints a predictable picture, writes Andrew Park, who assesses and analyses the figures.

Fresh data obtained on behalf of the Contentious Tax Group of tax dispute professionals casts light for the five years to 5 April 2025 on:

• the number of complaints made by taxpayers to HMRC;

• the number of those taxpayers receiving redress as a result of complaints;

• the total amount of redress paid by HMRC to taxpayers.

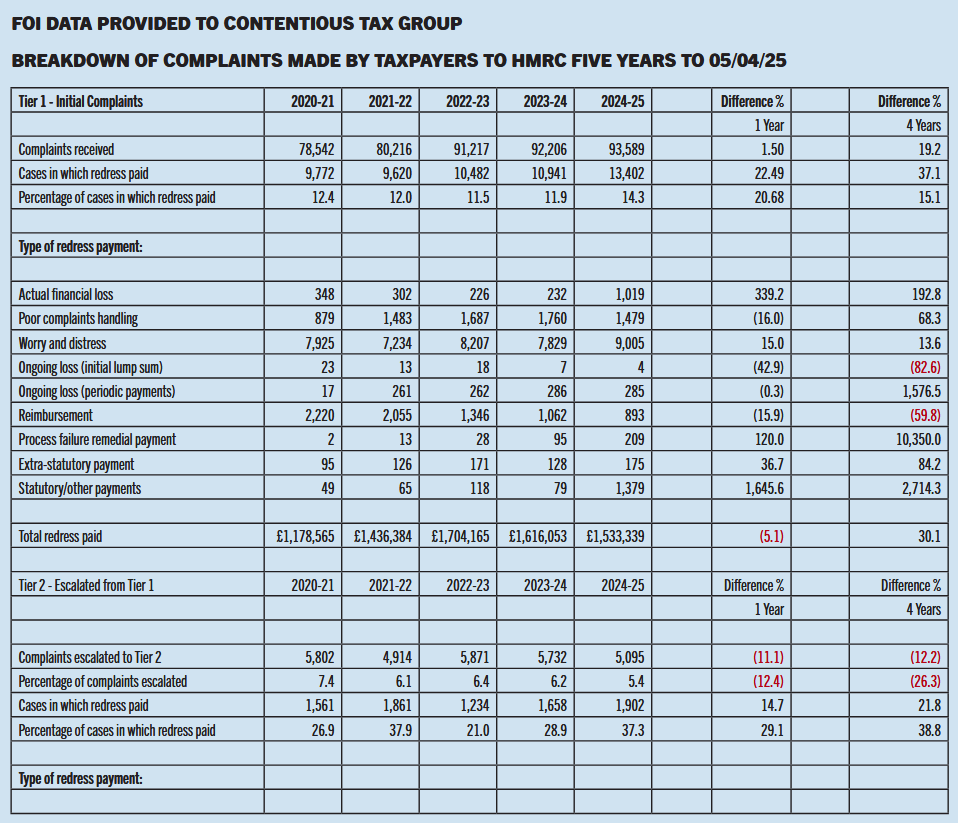

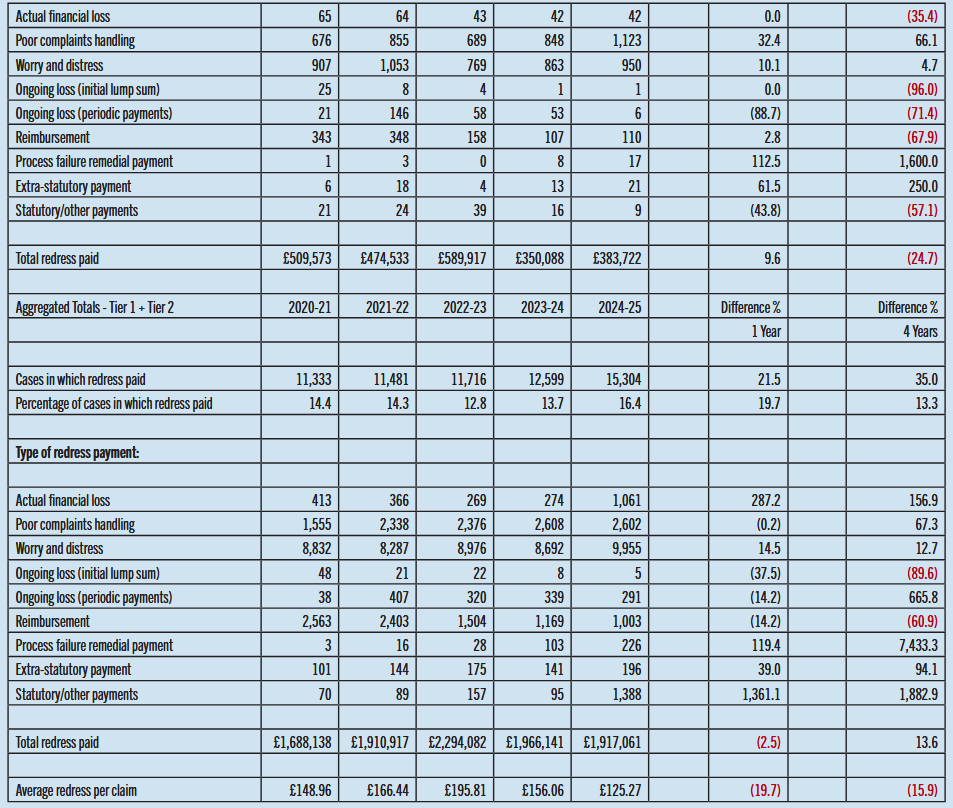

The HMRC data – together with additional rows analysing and aggregating it – is set out in the table here.

In providing the data HMRC explains: “We make redress payments to reimburse any actual financial loss or reasonable costs incurred as a direct result of our mistake and/or to acknowledge any distress and worry our mistake may have caused…

“The number of redress payments quoted reflects the number of cases in which we issued a payment. This figure does not necessarily match the number of customers whose complaints we upheld or partially upheld. For example, a single customer may have made more than one complaint during the tax year.

“Similarly, the breakdown of redress payments by type doesn’t equal the number of cases in which we made a payment. This is because we may pay redress for more than one reason in the same case. For example, we may pay an amount for worry and distress in addition to reimbursing reasonable costs.

“We have provided figures for complaints at both stages of our complaints process. Tier 2 complaints are escalations of Tier 1 complaints.”

It should be appreciated that, inevitably with HMRC data releases of this type, some variations are sudden and extreme and no inferences can be drawn because they point to changes in HMRC’s own categorisation methodology rather than shifts in fundamental truths. However, the data does reveal some clear trends and insights.

Uptick in complaints

Firstly, it will come as no surprise to this professional readership nor to the public that the total number of complaints has increased every year and by nearly a fifth over the whole five-year period. HMRC now receive nearly 94,000 formal complaints a year. Multiple independent reports over the past few years have pointed to a significant deterioration in HMRC service standards.

The Public Accounts Committee – which has had a particular focus on HMRC telephone response times as a readily measurable indicator, which on its own is a major complaints generator – reported in January 2025 that service was continuing to decline from an all-time low the previous year. More broadly but less readily measurable, professional advisors can attest to slower HMRC response times in written correspondence, a sense that HMRC is generally less well resourced and less productive and the increasing frequency with which HMRC staff are encountered who appear to lack sufficient basic training and capability. All of this translates into increased stress and anxiety for taxpayers and, all too often, financial hardship.

Where redress is paid

Not surprisingly, the rise in complaints to HMRC has gone hand in hand with an increase of over a third in the total number of cases for which HMRC has paid redress. Not only that, but the proportion of complaints cases in which redress has been paid has latterly increased too, and now stands at nearly 16% overall.

Falling levels of redress

It should be appreciated that HMRC redress payments are made on a purely ex gratia basis and are not intended to equate to the level of damages that might be awarded against HMRC in the courts. Potentially they can be very significant where material financial loss can be demonstrated but, in practice, the figures show that redress payments tend to be notional amounts towards minor additional costs inflicted on taxpayers for things like telephone calls, postage and sundry professional costs.

Notwithstanding the significant overall increase in the number of complaints made and the number of redress payments made, the total expenditure by HMRC on making the payments has remained comparatively stable and has trended downward in the past two years to just over £1.9m in 2024/25. The effect of that has been for average payments of only around £125 in 2024/25 compared with around £196 in 2022/23.

HMRC is making far more redress payments, but is balancing this with less generosity for what are, in the main, merely intended to be token gestures to taxpayers whose main motivation for making a complaint is seldom to seek financial redress. It is normally to get the service failure resolved – for instance, to get a repayment processed – and to get HMRC to accept and apologise for their shortcomings.

Quality of complaints handling

To HMRC’s credit, the data shows that only a small and falling proportion of complaints go unresolved at the initial Tier 1 stage and need to be escalated to Tier 2. Little more than one in 20 cases now need escalation and that proportion dropped from over one in 13 during the period. So it’s clear that, although HMRC service failures have become more frequent, the standard that HMRC have met on this measure in dealing with formal complaints has improved.

However, the number of redress payments in which poor HMRC complaints handling has been a factor has increased by over two-thirds over the period. So, it seems this is likely caused in large part by increasing poor handling of informal complaints by HMRC officers prior to taxpayers then having to go down the formal complaints process and make Tier 1 complaints.

Increasing distress to taxpayers

Although some categories of redress payment seem to have been subject to different HMRC methodologies over the period or are otherwise opaque, the unmistakable trend is that HMRC has had to accept that an ever-increasing number of taxpayers have suffered worry and distress as a result of HMRC actions or inaction. HMRC now accepts this in the cases of over 1,000 additional taxpayers a year compared with back in 2020/21 – taking the total number of taxpayers found to have suffered worry and distress meriting redress payments to nearly 10,000 a year.

What the figures don’t show

In practice, there are more ways to bring complaints to HMRC than through their official complaints reporting process. This is particularly the case in the context of ongoing enquiries or other forms of investigation – where complaints are often made to line managers or otherwise floated as ‘shots across the bow’ in order try to persuade HMRC to moderate difficult and unreasonable behaviour without it going far enough for HMRC to be obliged to log it as an official compliant.

The figures also don’t show the monetary success that taxpayer complaints – formal or informal – often achieve in persuading HMRC to give up on the unreasonable pursuit of tax or else to agree to tax refunds that otherwise wouldn’t have been forthcoming. Strictly, there is not supposed to be any connection between complaints about HMRC conduct and technical decisions about the correct amount of tax due – complaints are about behaviour and tax liabilities are appealable on their own merits based on the application of the law to the relevant facts, but inevitably sometimes the two interact.

The future

Not surprisingly, given the relentless level of scrutiny and criticism to which HMRC is subjected, HMRC has publicly committed itself both to improving its service standards such that fewer complaints are merited and to improve its complaints handling processes when complaints are made.

New technology is being offered up as a potential solution to reducing complaints and making complaints easier to bring. However, there are also suggestions that whilst technological improvements have yet to bear fruit HMRC has been deliberately withdrawing traditional means of customer support in order to herd taxpayers into the use of cheaper, de-humanised new digital pathways that aren’t yet fit for purpose.

For the moment, we know that in their interactions with HMRC taxpayers still want to deal with people – reasonable, accessible, competent people. HMRC’s own statistics show that increasingly often HMRC isn’t well enough organised and resourced to deliver that.

• Andrew Park, Tax Investigations Partner, Price Bailey